This guest blog was put together by Carl Abbott from Lift Insurance.

Under the 1969 Employers’ Liability (Compulsory Insurance) Act, most employers are obliged to take out Employers’ Liability Insurance against employee illness or injury.

The legislation requires employers to have at least £5 million of cover, purchased from an authorised insurer. Most insurers however offer a minimum of £10 million of cover to fully protect businesses.

Businesses can face severe penalties – currently £2,500 per day – if they don’t have the right policy in place. You can also be fined £1,000 if you do not display your EL certificate or refuse to make it available to inspectors when they ask.

Just take a moment and think about that… if your business doesn’t hold the right policy or level of cover this could cost your business over £900,000 per year in fines alone. Now think about the claim made against you, who’s paying the claim, who’s paying to defend the claim and who’s paying the compensation. Would your business survive this type of claim?

So how is your Employers Liability rated and why is it important to get it right the first time.

Insurers don’t always use the same rating structure, but the rule of thumb is very simple. The most common rating structure is per capita (per person) rated and wage roll, company turnover and trade.

Trade is very important because depending on the trade depends how the wage roll is rated. For example, the rate for an office worker will be less than a construction worker potentially working at height or depth. All aspects of insurance are based on the material facts (the information you supply). Using an Insurance Broker can reduce the risk of not supplying the correct information or misunderstanding the additional information required to fully protect your type of business. Getting it right the first time will protect your business and your employees in the event of a serious claim.

One example of not getting it right is as follows…

A building contractor was working exclusively for a limited business. Whilst at work the employee fell from a height of 15M seriously injuring himself. The director of the business failed to inform his insurer that his staff were working at height. As the insurers didn’t know about height at work they imposed an exclusion in the policy wording that any claim resulting from accidents at height was not covered. Given this, the insurer didn’t pay out on the claim and the business was made to pay damages to the employee at a cost of £169,990.

By simply telling the insurer or using a broker that fully understands your business needs, a claim like this would never have happened.

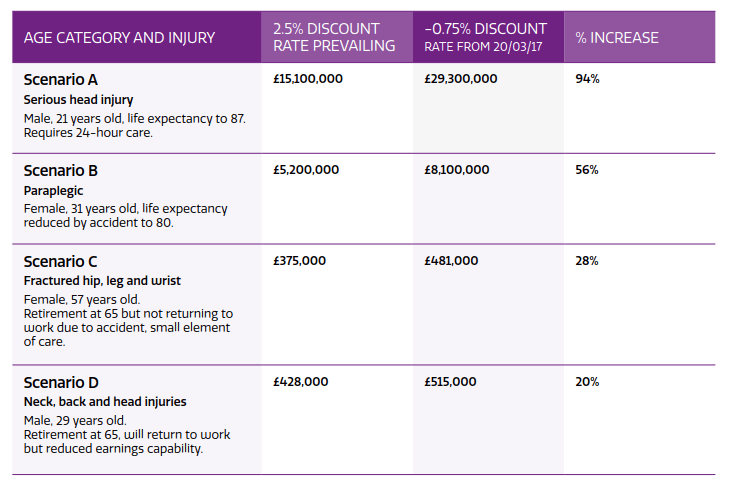

Under the New Ogden rating structure could your business survive not having the correct cover in place???

In summary, Employee Liability insurance is insurance that protects businesses. It covers businesses against injury to employees. We all hope we will never need to claim for this type of insurance, but you know what… if a claim ever does come in and it’s been done right and right the first-time round, this could be the best and most important thing your business has ever purchased.

_______

Your contact: Carl Abbott 0161 929 2626 / 07595 200990

carl.abbott@lift-insurance.com